Introduction

Whether it is the level of inflation, the direction of economic growth, credit quality in the consumer and corporate sector, the housing market, supply of US Treasuries, a slew of elections, geopolitics or even an outright stock market bubble, the list of investor worries and concerns during 2024 was as long as one can remember. Will the picture look any better for investors in 2025? The answer, perhaps predictably, is yes and no. Growth across the globe is slowing. Higher interest rates are taking their toll and consumers across most markets are tightening their belts. Meanwhile, heavy debt issuance across western developed countries leaves real rates vulnerable to shifting capital flows amid high geopolitical uncertainty.

These issues weigh heavily in the face of what is arguably the most pressing challenge in human history: climate change. Investors face a wall of worry and yet equity markets march on. Despite the uncertainties, there are causes for optimism. We appear on the verge of a further breakthrough in productivity, enabled by the ongoing evolution of computing platforms. We do not yet know how artificial intelligence (AI) will change society, but where there is change, there are opportunities for investors.

Perhaps the biggest risk to investors with time horizons of 10 years or more is missing out on the opportunities a well-diversified portfolio of global equities can offer. As a smart investor once said, “time in the market is far more important than timing the market”. This seems as true today as ever.

Three economic factors to consider in 2025

While we do not position ourselves as macroeconomic specialists, we remain cognisant that the stocks we invest in are not immune to broader economic factors. For us, headline risks such as US real interest rates, developments in China, and the AI capital expenditure cycle are key considerations. However, as we approach 2025, the trajectory of these issues remains uncertain.

1. US real interest rates

Given the context of challenging geopolitical conditions, trade barriers and the prospect of a heavy supply of US Treasuries, it may be prudent to assume that the level of real rates should be higher in the next decade than it has been for the last 10 years, meaning monetary settings would remain less supportive of growth. That said, banks, insurers, some industrials and potentially energy sectors could see their earnings prospects fare relatively well in this scenario. Given the advantageous valuation starting point, earnings upgrades for these industries could be accompanied by rising share prices. If this were to occur during a slowdown in the AI boom, these industries could take the lead in the market.

2. China’s economic outlook

Policy measures enacted thus far appear insufficient to prevent a potential debt deflationary cycle. We remain vigilant, but a sustainable shift in the narrative has yet to materialise. Without more aggressive fiscal spending, Chinese consumers are unlikely to alter their high savings rates.

3. AI adoption

The speed and scale of AI infrastructure development in 2023 caught many, including us, by surprise. The dominance of a narrow group of AI-related stocks seems to be fading, even as some continue to deliver strong growth. What had appeared to be the only growth ticket in town—AI spending—is now more difficult to assess. The hyper-scalers are delivering strong results, but the heavy capital burden and subsequent depreciation suggest that returns for some of these players may falter in 2025. Consequently, good stock picking will be key.

A Future Quality 2025 outlook

We do not yet know who the market leaders will be in 2025 and uncertainties continue to mount up. However, the only certainty is ever-accelerating change. In this environment, we believe diverse portfolios will win; our year-to-date winners have proven beneficial and we have renewed our focus on areas that are poised for longer term success. Our strategy remains to focus on businesses capable of sustaining and growing cash flow return on investment, often driven by unique management strategies that carve out competitive advantages.

One of our core investment principles is identifying companies that can expand market share in their respective industries. This capability often provides a competitive buffer against macroeconomic headwinds and industry-specific challenges as demonstrated by some insurance and consumer discretionary sector companies that were successful in 2024. Finding businesses that align with this theme has been a consistent area of focus for us, particularly in the healthcare sector, where data-driven insights are transforming outcomes and driving cost efficiencies.

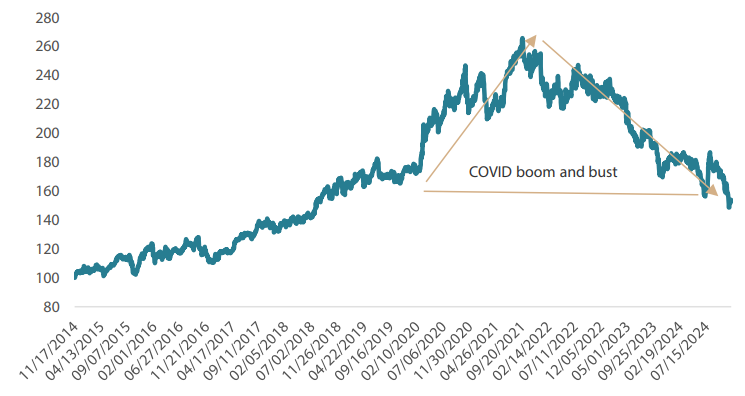

The healthcare sector’s performance has been mixed, particularly within the life science tools segment, which has experienced challenges following the extraordinary demand surge during the pandemic (Chart 1). These companies enjoyed robust compound growth from 2014 to 2019, driven by advances in scientific innovation and the development of personalised therapies targeting complex diseases such as Alzheimer’s, certain cancers and obesity. The unprecedented rush to develop and scale vaccines during the pandemic created a boom in demand, temporarily inflating growth rates and valuations.

Chart 1: Life science tools vs. healthcare*

*MSCI ACWI Life Sciences Tools & Services Index, rebased to 100 on 17 November 2014

Source: Bloomberg, as at 29 November 2024

However, a market correction took place from 2021 to 2023, realigning valuations more closely with long-term trends. This period also saw scepticism in the market about the sector’s ability to regain its pre-pandemic growth trajectory. However, we remain confident in the enduring demand for life science tools as the healthcare industry continues to prioritise innovation and personalised treatments. The long-term growth drivers for this sector—scientific advancements and rising demand for healthcare solutions—are intact, and we believe that life science tools companies are well-positioned for recovery in 2025.

Summary

The next 15 years are unlikely to be a repeat of the last 15, with the direction of real rates being the primary concern for investors. Our best guess is that we are now faced with a sustainably higher cost of capital than the abnormally low level we witnessed following the global financial crisis. This is influenced by a number of factors, including, but not limited to, the high forthcoming supply of government debt to fund a burgeoning fiscal deficit, the impact of geopolitics on trade restrictions and the inflationary implications of the energy transition.

From an investment perspective, looking for winners less exposed to such trends is always a critical part of finding genuine idiosyncratic alpha1, and this is more relevant today than ever before. If real rates are indeed set to rise over the next decade or so, this will have implications for stock picking as immediate profits become more valuable to investors than the hope of potential profit a decade from now. This might explain why the companies in the market related to the AI theme are performing so well, as they are also experiencing sharp increases in earnings and cash flow. This contrasts sharply with long-duration growth stocks, which continue to lag the market as the anticipated earnings for 2025 and beyond remain just that: hopeful prospects.

In a macroeconomic environment characterised by limited growth, identifying differentiated sources of revenue, profit margins, and cash flow becomes paramount. As bottom-up stock pickers, we have a diversified portfolio of Future Quality ideas. As we navigate an increasingly complex global environment, the richness of ideas across sectors like AI, healthcare, industrials, and defensive growth places us in a strong position to tackle the challenges and seize the opportunities ahead.

Throughout history, equity investors have benefitted from maintaining a long-term view and an optimistic outlook on humanity’s ability to prevail in the face of adversity. This might once again be the case, meaning that the biggest risk might be not having exposure to the highest quality earnings streams through a diversified portfolio of global equities.