This post was created in partnership with Nikko Asset Management Asia Limited. All views and opinions expressed in this article are Beansprout's objective and professional opinions.

Growing up, a well-worn copy of Robert Kiyosaki's "Rich Dad Poor Dad" sat on our family bookshelf.

You might know it. It's something of a bible for those seeking financial independence, telling the tale of two fathers and their contrasting approaches to money and wealth. In it, Kiyosaki paints his “rich dad” as a self-made multi-millionaire full of wealth-building wisdom.

The word “millionaire” has since become an ultimate benchmark–proof that you’ve “made it”. Yet, as I entered adulthood, having a million dollars in the bank felt about as realistic as growing wings and flying.

Despite having Kiyosaki's wisdom literally within arm's reach at home, my family was decidedly in the "poor dad" category. Moreover, my first job out of university paid a humble $1,000 per month.

Saving towards a million just wasn’t on the cards for me, and it seemed like my starting point set me miles behind the coveted seven-figure mark.

But as I progressed through adulthood, I developed habits, mindsets, and behaviours that transformed my financial trajectory. These days, I believe that the million-dollar mark is no longer a question of if, but when.

Breaking down the math and mindset to $1M

Building a million-dollar net worth isn't a novel aspiration. Spend five minutes on r/SingaporeFI (reddit) and you'll see countless discussions on this topic. With today's rising cost of living and the growing desire for financial freedom, it's easy to understand why this figure has become such a common target.

So let’s put this $1M milestone in concrete terms:

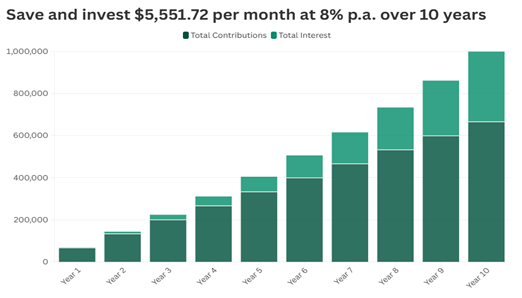

Say you start working at 25 and set a goal to hit $1M by 35. That gives you a 10-year time horizon. Assuming an 8% annual return, you’d need to save and invest $5,551.72 per month.

Source: Beansprout, 14 February 2025. Average annual returns of 8% is for illustrative purposes only.

For most people, this is a stretch.

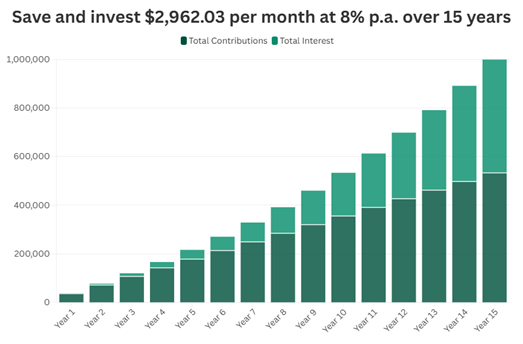

Now, let’s extend the timeline. What if we aim for $1M by 40 instead? With a 15-year time horizon and the same 8% annual return, you’d need to save and invest $2,962.03 per month.

Source: Beansprout, 14 February 2025. Average annual returns of 8% is for illustrative purposes only.

Still substantial, but now the numbers don't immediately make you want to give up. (And this is before we even factor in CPF contributions or property assets.)

This is also where it is important to make a quick note about mindset.

Since hitting $1M is mathematically possible, we may sometimes think that focusing on the number is all that matters.

Yet we also know that life isn’t linear. It rarely follows our neat little spreadsheet calculations.

Rather, it's about developing the habits, mindset, and strategies that make $1m achievable.

Unexpected expenses, job changes, family commitments, and market downturns will impact your trajectory. That’s why focusing only on the number can miss the bigger picture.

Think about it this way: even if you fall short of that million-dollar mark, developing strong financial habits puts you leagues ahead of where you'd be otherwise.

The three levers of building wealth

On my journey to building wealth, I've discovered there are three main levers you can pull:

- Accelerating your income

- Developing a savings habit

- Investing consistently

Let’s break them down.

#1 – Accelerating income

No amount of budgeting would turn my measly $1,000 salary into serious wealth. Something had to change. And that something was my income.

In the early days of my career, that meant juggling side hustles like tuition gigs, upskilling with professional certifications, and strategically negotiating salaries to land higher-paying jobs.

Every extra dollar earned was a step closer to that million-dollar goal.

But while side hustles are great for quick wins, the real power lies in taking a long-term view of your career growth.

Focus on developing high-income skills that compound over time, skills that would make employers think twice about letting you go, or better yet, compete to hire you.

This means asking yourself questions like:

- What value am I bringing to my employer?

- How can I make myself indispensable?

- Where are the gaps in my skillset that are holding me back from that next big promotion?

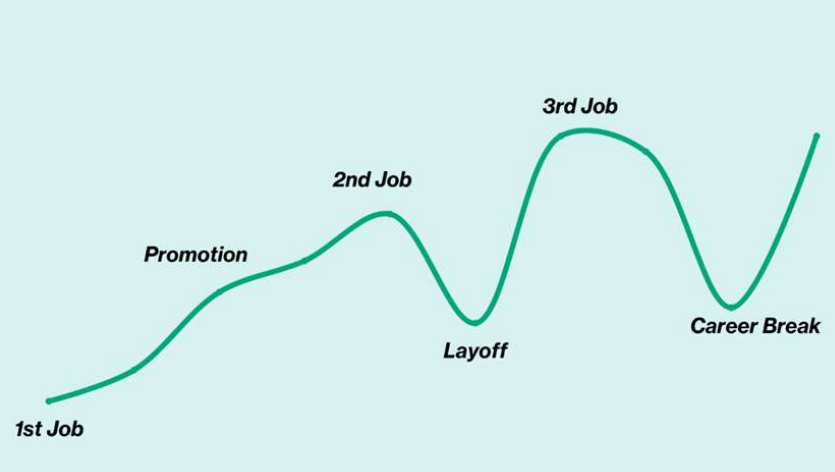

The journey isn't all upward. You might hit your fair share of walls. Career switches and industry shifts could feel like you’re starting over. You might even face periods of burnout.

But setbacks aren’t necessarily obstacles; they could be opportunities in disguise. Facing these setbacks head-on develops resilience.

Sometimes, the path to higher income may be a series of strategic zigzags that eventually lead you to your goal.

Source: Beansprout

#2 – Building a savings habit

Saving money isn't exactly exciting. But if you're serious about that million-dollar goal, you have to be intentional about it.

I'll be the first to admit that being disciplined with savings can feel like swimming upstream.

There's always another milestone to celebrate, another vacation to plan, another trendy restaurant to try. Life serves up endless opportunities to part with your money.

But think of saving as buying freedom for your future self.

Every dollar you save gives you options.

Options to take that dream job even if it pays less initially. Options to start a business. Options to say "no" to things that don't align with your values.

To me, the key is making it automatic.

Treat savings like a non-negotiable bill. It's the first "expense" that gets paid when my salary hits my account. No thinking required. No willpower needed. Just an automatic transfer that happens before I can talk myself out of it.

You don’t have to obsessively track every expense either. Do regular check-ins to understand your spending patterns.

Have a conversation with your money rather than interrogate it:

- Where are the leaks?

- What adjustments make sense?

- What spending brings value to my life?

You don't need to be perfect at saving. You just need to start. It's okay if you slip up sometimes. What matters is building the habit and staying consistent over the long run.

Once you build this habit, it becomes second nature. The mental struggle fades and the fear of missing out (FOMO) lessens. And gradually, your wealth grows in ways that feel almost effortless.

#3 – Investing consistently

Saving money alone won’t get you far.

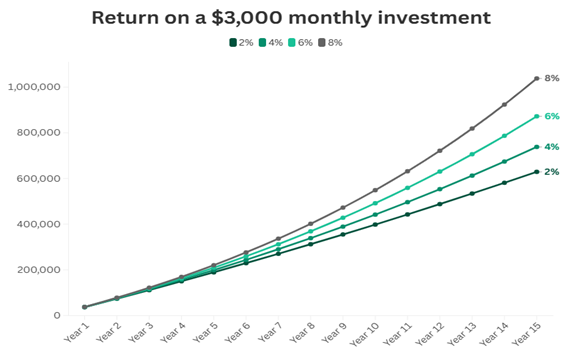

If you’re setting aside $3,000 a month in an account that yields just 2% per year, it’ll take over two decades to hit $1 million.

While that’s still a decent outcome, for those aiming for financial independence earlier in life, that timeline might feel painfully slow.

I believe that this is where investing becomes crucial to the $1 million journey. Compounding accelerates your path to wealth, especially when you start early and stay consistent.

Here’s how much your wealth can grow at different return rates:

Source: Beansprout, 14 February 2025. Average annual returns of 2%-8% is for illustrative purposes only.

But sticking to an investment habit is easier said than done.

Dollar-cost averaging (DCA), investing a fixed amount regularly to smooth out market volatility and build a savings habit sounds great in theory but in practice, it can be tough.

When the market is booming, it’s tempting to throw in more money out of FOMO.

When it’s crashing, the urge to pull out and ‘wait for things to settle’ is real. Emotions make terrible investment advisors.

That’s why automation is your best friend. Setting up a Regular Savings Plan (RSP) takes emotions out of the equation.

If you don’t have the time or expertise to pick individual stocks, you could invest in ETFs through an RSP.

An ETF is a low-cost way to own a diversified basket of securities. Instead of buying individual stocks, ETFs allow you to invest in a broad market index at a lower cost.

For example, buying the STI Index ETF gives you exposure to the top 30 stocks by market capitalisation in Singapore—without needing to buy each stock individually. This means built-in diversification and lower risk compared to picking individual stocks.

Here are some Singapore-listed ETFs you can consider for dollar-cost averaging:

Your investments keep flowing in with an RSP, whether the market is up, down, or sideways.

It becomes just another monthly ‘expense’, except this one is silently building your future wealth.

Learn how Regular Savings Plans work and the ETFs you can consider for long-term investing.

Less a goal, more a way of life

While I’ve set out to hit $1 million, I’m well aware of the things out of my control that might cause me to miss the mark.

Life circumstances, unexpected challenges, market downturns, and competing priorities can change the trajectory of my financial journey. And that’s okay.

What matters more is aligning your financial goals with what brings you long-term happiness.

If hitting $1 million means sacrificing things that genuinely fulfil you like spending time with family, pursuing a passion, or giving your child the best education, then it’s worth asking: Is that number really the goal?

At its core, the journey cultivates the $1 million mindset and reinforces it with habits that build wealth over time. It's like training for a marathon. Even if you don't finish first, you're still far more fit than if you'd never started training at all.

Whatever your financial goal may be, the principles remain the same:

- Develop tenacity to find ways to increase your income

- Build a disciplined savings habit

- Invest strategically and consistently to grow your wealth

If you’re looking for a place to start, a Regular Savings Plan (RSP) through ETFs can be a simple way to automate your investments and set the foundation for long-term growth.