Why you need to invest your SRS funds

In this era of high-yield savings accounts offered by banks, did you know that our SRS funds yield only 0.05% p.a.? If you want to protect your SRS funds from losing purchasing power due to inflation, consider investing in ETFs, which can potentially offer higher returns.

Disclosure: This post is brought to you in collaboration with Nikko Asset Management. All research and opinions are that of my own, and should not be taken as financial advice for your specific situation(s) as I know nothing about your individual financial circumstances, risk tolerance or investment objectives. I highly recommend that you use this as a starting point to understand more about the various ETFs offered by NikkoAM which you can use for SRS investing, and then click into the respective links above to retrieve the fund prospectus and performance so as to help you decide whether it fits into your investment objectives.

With the year coming to an end, some folks are topping up their Supplementary Retirement Scheme (SRS) accounts to reduce their tax bill when It is time to file tax returns in the new year.

If you’re trying to do the same, remember to complete your funds transfer within this month – by 31 December of each year – in order to qualify for the tax relief on your tax bill served to you in April.

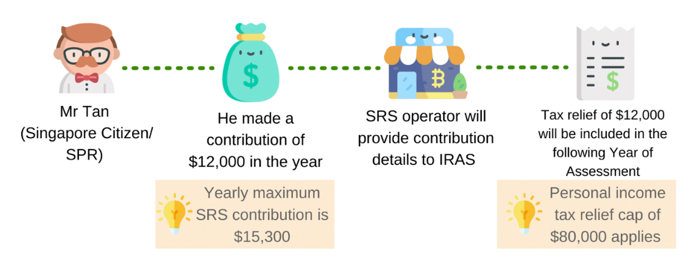

Image credits: Sourced from IRAS website on SRS, November 2024. The maximum yearly SRS contributions that one can make is $15,300 for Singaporeans and PRs, while the cap is higher at $35,700 for foreigners.

A key driver of this success is China’s robust EV infrastructure, including an extensive network of charging and battery-swapping stations.

Cities like Beijing and Shanghai have implemented zero-emission vehicle mandates, accelerating the shift to EVs by restricting the sale of internal combustion engine (ICE) vehicles.

But what happens after you top up your SRS?

If you’re guilty of leaving the funds idle in your account, that’s a big missed opportunity because over time, inflation alone would negate any tax benefits you get from contributing to your SRS account. Your money not only loses its purchasing power each year, but you’re also missing out on the chance to have grown the money for higher returns that may earn you more than just 0.05% per annum. However, you will need to be aware of and manage the investment risks of being exposed to the financial markets when you put your SRS monies to work, vs leaving it in your bank account to earn 0.05% pa interest.

Even though most banks have raised their interest rates over the last few years, this does not apply to your SRS account. Go ahead and check – you’re still only earning 50 cents for every $1,000 saved. If you had maximized your SRS contributions to reduce your income tax, that’s only $7.65 on every $15,300!

If you asked me, I think it is silly to just contribute to your SRS account; you will need to invest your funds as well.

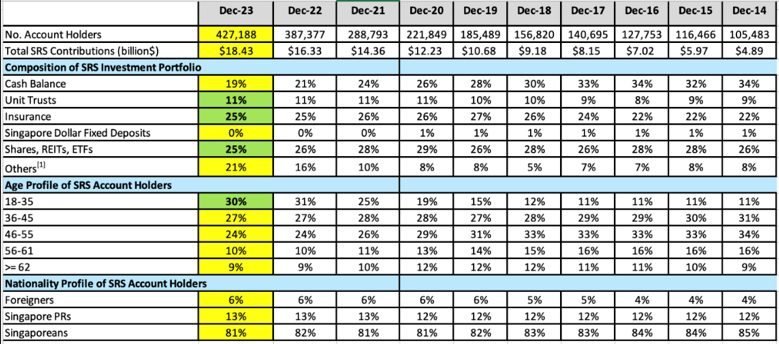

What do people invest their SRS funds in?

To get an idea of what most people invest their SRS money in, you can refer to these statistics released by the Ministry of Finance here, which shows that the most popular tools used are:

- insurance (25%)

- stocks, real estate investment trusts (REITs) or exchange traded funds (ETFs) (25%)

- Singapore Government Bonds, Corporate Bonds, Foreign Currency Fixed Deposits and Fund Management (Others) (21%)

- unit trusts (11%)

Source: The Ministry of Finance, November 2024

[1] “Others” comprise of Singapore Government Bonds, Corporate Bonds, Foreign Currency Fixed Deposits and Fund Management

Single Premium Insurance Policies

Buying a single premium insurance plan has typically been a very popular option among SRS account holders. These are usually your endowment or annuity plans, which are sold by insurance agents and are designed to provide a lump sum payout at maturity or a steady stream of income in the future, starting from a date* of your choice. Its attractiveness lies in the fact that a portion of investment returns is usually guaranteed, which explains why such insurance plans have traditionally been well-received among those who are more conservative.

*Sidenote: you might want to set a date after you turn 62 years old, or later. This is so you won’t incur the 5% early withdrawal penalty and be subjected to only 50% of the withdrawn amount being taxable.

Stocks, REITs or ETFs?

If you’re looking for investments with lower fees, then buying individual stocks, REITs or ETFs directly from an exchange might be more of your cup of tea as compared to non-listed products.

And if you prefer not to manage individual counters, then investing through ETFs can provide a cost-effective approach that also takes less time to analyse and monitor. A single ETF can help you achieve diversification as you are exposed to different companies and industries, and diversification can often help to dilute volatilities coming from the individual stock counters. .

For example, the Nikko AM Singapore STI ETF –tracks the top 30 companies listed on the SGX-ST Mainboard ranked by full market capitalisation.– and has a low total expense ratio (TER)of 0.26% p.a (audited as of financial period ended 30 June 2024) and the ETF has a TER cap of 0.25% p.a.2.

Over the long-run, especially if you intend to invest long-term for your SRS monies before withdrawing them in your retirement years, putting this sum to work will help avoid having its value being eroded by inflation.

Bonds

1 in 5 SRS account holders have currently invested their monies in bonds, which generally come issued with fixed maturity dates, allowing you as an investor to know when you can expect to receive your principal back. What’s more, bonds are popular for their fixed income payouts (known as “coupons”) which goes back into your SRS account.

Some examples of bonds that you could invest in with your SRS funds are the Singapore Government Securities (SGS) bonds and Treasury Bills (T-Bills), which have a minimum application amount of S$1,000 and is subject to a $2 transaction fee.

If you prefer to invest in a basket of bonds rather than manage individual bond positions yourself, then other alternatives you could look at include the ABF Singapore Bond Index Fund which invests mainly in Singapore government/government-linked bonds, or the Nikko AM SGD Investment Grade Corporate Bond ETF which tracks the iBoxx SGD Non-Sovereigns Large Cap Investment Grade Index, which is made up of investment grade bonds issued mainly by established and credible Singaporean companies (such as DBS and Singtel)* and Singaporean statutory boards.

*as of 31 October 2024

Check out this article: Are Bond ETFs worth investing in?

Unit Trusts

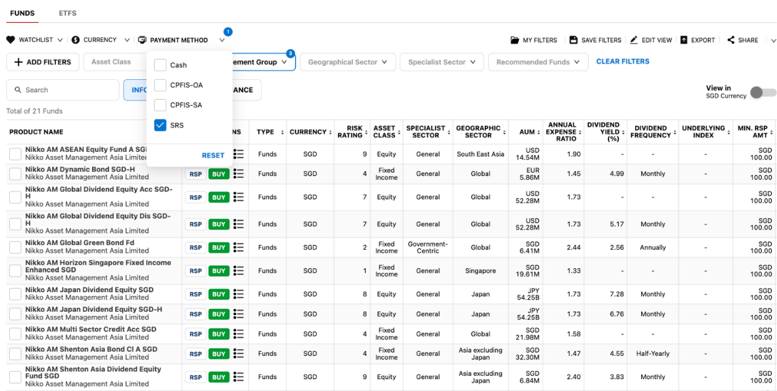

As you can see from the table, unit trusts are another option that SRS investors go for. A quick search on FSMOne’s Funds & ETF Selector with “SRS” selected as the payment method will show up its entire universe of approximately 1,230 funds for investors to choose from.

Source: Screenshot from FSMOne Funds & ETF Selector

These unit trusts are actively managed by a fund manager. As such, active management fees will apply.

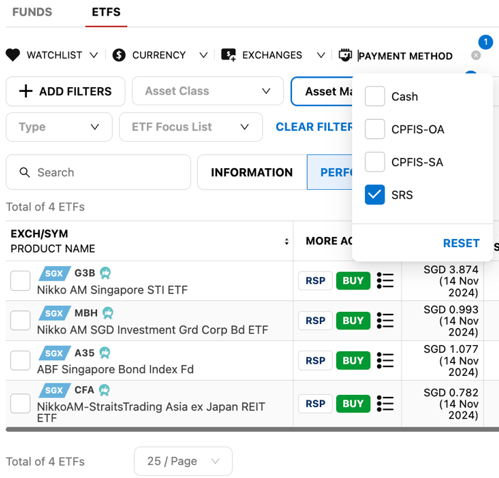

What ETFs can I use my SRS funds for?

Your SRS monies can be used to purchase any ETFs listed on SGX, where there are currently over 70 types of ETFs that you can choose from. You can use a stock screener such as FSMOne’s Funds & ETF Selector to filter through and see what makes sense to you (see below screenshot).

Some of the more prominent names include the Nikko AM Singapore STI ETF, which has a 1-year return of 21.92% as of 31 Oct 2024,* or the NikkoAM-Straits Trading Asia ex Japan REIT ETF that has consistently been paying distributions 4 times a year, for the past 7 years^.

*Returns are calculated on a NAV-NAV basis and assuming all dividends and distributions are reinvested, if any. Past performance is not indicative of future performance. Please refer to the Fund factsheet for the full range of returns.

^Distributions are not guaranteed and are at the absolute discretion of the Manager. Any distribution is expected to result in an immediate reduction of Fund’s NAV. Distributions may be paid out of capital which will result in capital erosion and reduction in the Fund’s NAV, which will be reflected in the redemption price of the Units.

The fees you pay for such passively-managed funds are generally low. Here’s the total fund fees investors can expect to pay on the above 4 funds:

|

|

Total Expense Ratio (p.a.)

|

|

ABF Singapore Bond Index Fund

|

0.25%[1]

|

|

Nikko AM Singapore STI ETF

|

0.26%[2]

|

|

Nikko AM SGD Investment Grade Corporate Bond ETF

|

0.26%[3]

|

|

NikkoAM-StraitsTrading Asia ex Japan REIT ETF (SGD Class)

|

0.55%[4]

|

However, note that aside from the total expense ratio, you will also incur brokerage fees each time you make a buy or sell transaction. To minimize this, some SRS investors may choose to invest only once or twice a year, but if you prefer not to try timing the markets and do dollar-cost averaging instead, then you can set up a Regular Savings Plan (RSP) to consistently invest your SRS monies every month, regardless of the trading price.

Visit Nikko AM ETF site to find all their ETFs. There are 4 Nikko AM ETFs which you can invest using your SRS :-

https://www.nikkoam.com.sg/funds/abf-singapore-bond-index-fund

https://www.nikkoam.com.sg/funds/nikko-am-sgd-investment-grade-corporate-bond-etf

https://www.nikkoam.com.sg/funds/nikko-am-singapore-sti-etf

https://www.nikkoam.com.sg/funds/nikkoamstraitstrading-asia-ex-japan-reit-etf-sgd-class

To read more about how to invest using SRS, visit How to invest in ETFs using SRS

TL;DR Conclusion

Regardless of your preferred frequency, it is important to note that allowing your SRS funds to remain idle in your bank account may result in missed opportunities for potential growth.

If you’ve been procrastinating, Budget Babe is telling you now: make today the last day you do so.

Note: While ETFs provide a fuss-free way to invest, you should note that all investments are not without risks. Specifically, key risks of the ETFs mentioned include market and credit risks, liquidity risks, product-specific risks including tracking error risks, risk associated with the investment strategy of the Fund or a lack of discretion by the Manager to adapt to market changes, emerging market risks (in addition for the ABF Singapore Bond Index Fund), and interest rate risk and credit risk (in addition for Nikko AM SGD Investment Grade Corporate Bond ETF). Investments in the Fund may also be exposed to other risks of an exceptional nature from time to time. Please refer to the Fund Prospectus and Product Highlights Sheet for further details.