This article was written in collaboration with Nikko Asset Management. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

Planning for retirement might not seem urgent today, but it’s one of the most crucial aspects of financial planning that none of us can afford to overlook. After all, unless we plan on working forever (and have the ability to do so), there will come a time when we’ll need a stable income to support us in our later years.

In Singapore, our Central Provident Fund (CPF) and Supplementary Retirement Scheme (SRS) savings are designed precisely for this—providing a structured path to build and grow a comfortable retirement nest egg. These schemes ensure that when the time comes, we have enough savings to sustain the lifestyle we want, covering daily essentials and enabling us to enjoy the lifestyle that we wish to pursue.

To encourage proactive planning, the government offers attractive tax relief for contributions to CPF and SRS accounts. This includes up to $8,000 per year for topping up your own CPF account, plus an additional $8,000 for topping up family members’ accounts. For SRS contributions, Singaporeans and PRs can get relief on up to $15,300 per year, while foreigners can enjoy relief on up to $35,700.

But here’s the thing: saving alone, even with tax relief, often isn’t enough. To truly supercharge our retirement funds, we may need to go beyond just saving—we may need to invest. By putting both our SRS and CPF savings to work through smart investments, we may potentially grow our retirement fund faster, thereby building a future we can look forward to.

SRS Vs CPF: Understanding The Differences

Before jumping into topping up our SRS and CPF accounts or investing our savings, it’s essential to understand a few key differences between these schemes. While CPF contributions are mandatory for Singaporeans and Permanent Residents (PRs), the SRS is a voluntary scheme, available to foreigners as well as Singaporeans and PRs.

One major distinction between CPF and SRS lies in their respective interest rates. CPF savings automatically earn a base interest of at least 2.5% per year in the Ordinary Account (OA), providing a stable, risk-free return. In contrast, uninvested SRS funds left in a bank account yield a minimal interest of just 0.05% annually. This creates a stronger incentive to invest our SRS savings, as leaving them idle in a bank account does little to grow our wealth.

With SRS, we need to take a proactive approach, exploring investment options that suit our risk tolerance and retirement objectives. While CPF provides a steady interest rate, investing CPF savings may also be a strategic way to grow our retirement fund. If we feel confident in earning a higher return than the OA’s 2.5%, then investing those funds could make sense. By carefully selecting appropriate investments, we might grow our retirement savings more effectively, ultimately increasing the funds available for our future lifestyle. At the same time, we must also be aware of the investment risks of investing our SRS and CPF savings and investing our monies means being exposed to the risk of the financial markets.

Investing Our SRS & CPF Savings Through ETFs

A practical way to kick-start investing is through Exchange-Traded Funds (ETFs). Like individual stocks, ETFs are traded on exchanges like the Singapore Exchange (SGX), but each ETF holds a diversified basket of assets, which might include stocks, bonds, and real estate investment trusts (REITs). By investing in a single ETF, we gain immediate exposure to a wide array of companies or bonds, which helps spread risk and balance out fluctuations across individual assets.

For long-term investors, this built-in diversity can be particularly advantageous, as it reduces the impact of any single security’s ups and downs, providing a more stable foundation for growing our retirement nest egg. ETFs also suit those who prefer a more hands-off approach to investing. Since most ETFs follow a specific index or strategy, there’s less need for constant monitoring or frequent adjustments—making them a lower-maintenance yet effective option.

On the SGX, we have access to various ETFs that we can easily invest in with our SRS and CPF savings. Whether our interests lie in global markets, specific sectors, or a balanced mix of stocks and bonds, there’s likely an ETF that aligns with our investment strategy, offering a simple and efficient way to work toward our retirement goals.

Invest In ETFs Listed on The SGX

For instance, if you're seeking broad exposure to Singapore's leading companies, the Nikko AM Singapore STI ETF (SGX: G3B) is a compelling option. This ETF seeks to mirror the Straits Times Index (STI), which tracks the performance of the top 30 companies listed on the SGX by market capitalisation.

By investing in this ETF, you gain access to a diversified portfolio that includes major corporations such as DBS, OCBC, UOB and Singtel (as of October 2024).

Fund Holdings

Source: Nikko AM Singapore STI ETF, October 2024 Factsheet

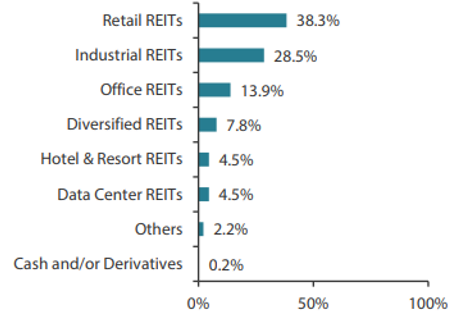

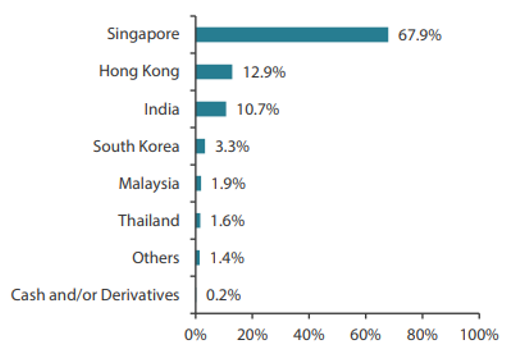

If you're aiming to invest in a diversified portfolio of Real Estate Investment Trusts (REITs) for regular distribution income, the NikkoAM-StraitsTrading Asia ex Japan REIT ETF - SGD Class (SGX: CFA/COI) is a possible option.

This ETF provides exposure to leading REITs in Singapore, such as CapitaLand Integrated Commercial Trust and CapitaLand Ascendas REIT. Additionally, it offers access to major REIT markets across Asia, including Hong Kong and India, with holdings like Link Real Estate Investment Trust and Embassy Office Parks REIT (as of October 2024).

Fund Holdings

Sector Allocation

Country Allocation

Cash in allocation charts includes cash equivalents. Percentages of allocation may not add to 100% due to rounding error

Source: NikkoAM-StraitsTrading Asia ex Japan REIT ETF - SGD Class, October 2024 Factsheet

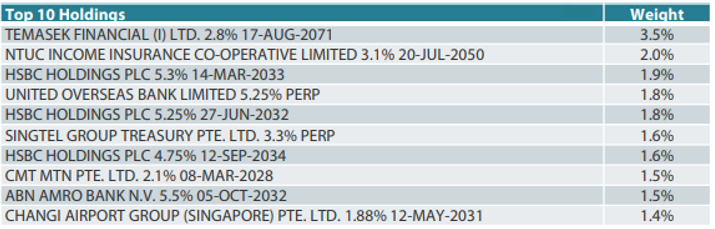

For those seeking bond exposure so that we can enjoy steady income, the Nikko AM SGD Investment Grade Corporate Bond ETF (SGX: MBH) offers an attractive option. By investing in this ETF, we gain access to high-quality corporate bonds issued by well-established entities such as Temasek, NTUC Income, DBS, HSBC and UOB (as of October 2024).

Fund Holdings

Source: Nikko AM SGD Investment Grade Corporate Bond ETF, October 2024 Factsheet

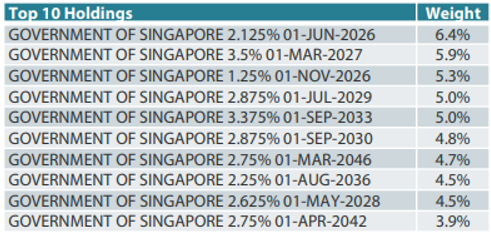

Alternatively, the ABF Singapore Bond Index Fund (SGX: A35) is a solid choice for investors prioritising safety and creditworthiness. This fund mainly includes bonds issued by the Singapore government, which boasts a AAA credit rating (as of October 2024), along with bonds from Singapore quasi-government entities.

Fund Holdings

Source: ABF Singapore Bond Index Fund, October 2024 Factsheet

Beyond the ETFs we've highlighted, there are many other options on the SGX for investors looking to diversify. In fact, SRS funds can be used to purchase any ETF listed on the SGX (find out more about investing in ETFs using SRS here). This means that if we’re interested in a specific sector or market outside of Singapore, we can leverage our SRS savings to invest in ETFs that provide exposure to those areas.

For CPF, the eligible ETFs are more selective, and the complete list can be found on the CPF website.

Of course, it’s important to point out that investing our SRS and CPF savings comes with investment risks as the financial markets can be volatile. If we do not have the knowledge to invest well, or do not have a long enough investment horizon to ride the ups and downs of the market, we could lose our capital in the market. Thus, if we wish to invest our SRS and CPF savings, we need to ensure that we are equipped with the right knowledge to make good investment decisions.

To learn more about Nikko AM ETFs, visit the NikkoAM website for resources on unlocking the potential of ETFs for your investment goals.

Read Also: Together As One: 4 ETFs Listed On the SGX That Allow You To Invest In Singapore’s Economy

What are the key risks of the Funds?

- Market and credit risks

- Liquidity risks

- Product-specific risks

- Tracking error risk

- Risk associated with the investment strategy of the Fund/lack of discretion by Manager to adapt market changes

- Emerging market risks (in addition for ABF Singapore Bond Index Fund)

- Interest rate risk and credit risk (in addition for Nikko AM SGD Investment Grade Corporate Bond ETF)

You should be aware that investment in the Funds may be exposed to other risks of an exceptional nature from time to time. Please refer to the Fund Prospectus and Product Highlights Sheet for further details.